Tight Balance amid Policy Disruptions: A Comprehensive Review of the Tin Market in H1 2025

I. Price Trends and Core Drivers

In H1 2025, tin prices exhibited a pattern of "jumping initially, then pulling back, and finally fluctuating rangebound." At the beginning of the year, influenced by the delay in the resumption of production at mines in Myanmar's Wa State, the supply of tin concentrates remained tight, driving LME tin prices up from $24,000/mt to a three-year high of $38,395/mt in March. However, in April, the implementation of the US's "reciprocal tariff" policy, coupled with the phased resumption of production at the Bisie mine in the Democratic Republic of the Congo (DRC), led to a rapid price pullback to 240,000 yuan/mt (SHFE tin) and $28,925/mt (LME). In May-June, due to the lag in the resumption of production in Myanmar and Thailand's suspension of transit transportation for Myanmar's tin ore (reducing monthly supply by 500-1,000 mt), prices rebounded again, fluctuating rangebound between 280,000 yuan/mt (SHFE tin) and $33,500/mt (LME). The cumulative increase in LME tin prices for H1 was 16.03%.

II. Supply Side: Tight Ore Supply, Shrinking Ingot Output, and Pressure on Smelting

Deepening Shortage of Tin Concentrates:

China's imports of tin concentrates from January to May were only 50,200 mt, down 36.6% YoY, mainly due to an 80% drop in supply from Myanmar. The resumption of production in Wa State was hindered by aging mine shafts, an early rainy season, and Thailand's transportation ban. Annual production is expected to decrease by 3,000 mt compared to 2024.

Although the Bisie mine in the DRC resumed production, its annual production guidance was lowered from 20,000 mt to 17,500 mt.

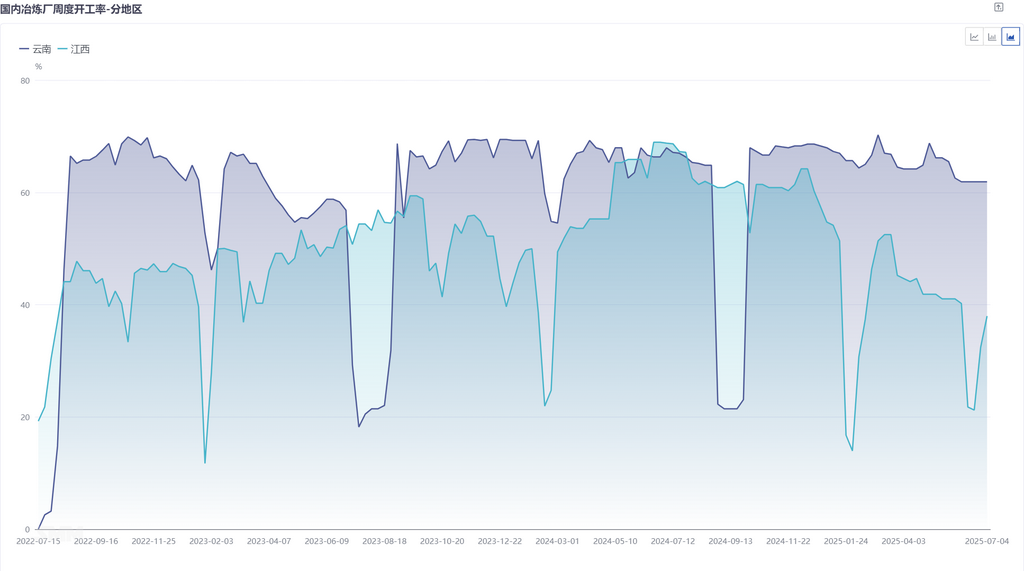

TCs Continuously Hit Bottom: The TCs for 40% tin concentrates in Yunnan dropped to 11,000 yuan/mt, and those for 60% concentrates in Jiangxi fell below 8,000 yuan/mt.

Some smelters were forced to undergo maintenance due to raw material inventories lasting less than 30 days. The operating rates of smelters in Yunnan and Jiangxi remained at around 50%.

Shrinking Smelting Output: Domestic refined tin production from January to June was 88,900 mt, down 3.6% YoY. Although imports of tin ingots increased by 30.91% YoY, the increase was limited after the import window closed.

The tight ore supply has been transmitted to smelting. It is expected that production growth in H2 will depend on the resumption of production and increased output from Myanmar by the end of Q3.

III. Demand Side: Resilience from Electronics, Weakening New Energy Demand

PV Industry: After the installation rush ended, orders for PV tin strips in east China declined, and the operating rates of some producers decreased;

Electronics Industry: Electronics terminals in south China entered the off-season. Coupled with high tin prices, end-users had a strong wait-and-see sentiment, and orders only met immediate needs;

Other Sectors: Demand in sectors such as tinplate and chemicals remained stable, without unexpected growth.

IV. Inventory: Global Spot Inventory Continues to Decline, with Limited Overall Replenishment

LME inventory decreased by 50% in H1. SHFE inventory fell to 7,198 mt, and social inventory also dropped to 9,754 mt, supporting the structure of spot premiums.

V. H2 Outlook: Tight Balance to Persist

Price Range: LME tin is expected to trade within $30,000-36,000/mt, SHFE tin within 245,000-290,000 yuan/mt. Low inventory and policy dividends provide resilience, but caution is warranted against the combined pressure of Q4 restocking completion and off-season inventory buildup.

Summary:

In H1 2025, the tin market exhibited high volatility amid "tight ore supply and reduced ingot output" and "divergent consumption," with prices showing pronounced event-driven characteristics. The H2 supply-demand weakness persists, but low inventory and resilient electronics demand may support the price center. Vigilance is advised against Q4 downside risks stemming from Myanmar's production resumptions and macro headwinds.

![The Most-Traded SHFE Tin Contract Opened Lower and Then Traded Stronger, Spot Market Recovers Amid Downtrend [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/WWXJU20251217171753.jpg)

![The most-traded SHFE tin contract fluctuated rangebound during the night session, with downstream enterprises mostly following up with small-lot transactions. [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)